Ask most people how interest rate impact on Singapore property prices and you’ll get the same answer every time. Rates go up, prices come down. Rates go down, prices climb. Clean, simple, done.

Except that’s not what actually happened here. We went digging through 21 years of price data to see if this “obvious” relationship holds up, and honestly, it doesn’t hold up nearly as well as people assume. The link between interest rates and Singapore property prices is a lot messier once you actually look at the numbers instead of the theory.

TL;DR

- Interest Rate Impact on Singapore Property Prices isn’t as direct as most people think. Prices have risen during several periods when rates were climbing too.

- Transaction volume tracks interest rates far more reliably than price does. Cheap borrowing brings more buyers and sellers into the market, not necessarily higher prices.

- SORA is sitting around 1.0-1.2% as of mid 2026, down sharply from over 3.5% back in 2023. Fixed mortgage packages now start from roughly 1.40%.

- Land supply, immigration policy, and cooling measures like TDSR and ABSD do more to shape Singapore property prices than interest rate movements ever have.

- A 1% swing in your mortgage rate on a $1 million loan adds up to about $480 extra a month, or close to $144,000 over 25 years.

- Most analysts are expecting 2-5% growth in private home prices for 2026, helped by cheaper mortgages rather than caused by them.

How Interest Rate Impact on Singapore Property Prices Are Actually Connected

Interest rates touch three things directly. What it costs you to borrow. How property compares to other places you could park your money. And how confident buyers feel about committing to a loan they’ll be paying off for the next 25 years.

Drop mortgage rates, and monthly repayments drop too. More people qualify for bigger loans, and a chunk of buyers who’d been dragging their feet suddenly decide it’s time to act. That’s the affordability piece, and it’s genuinely real.

Push rates up, and the theory says the opposite should happen. Borrowing costs more, some buyers get squeezed out, demand cools. Fair enough, that logic works fine on paper.

But here’s the thing. Singapore’s actual price history over the past two decades doesn’t play along with that story nearly as much as you’d expect.

What Actually Drives Singapore’s Mortgage Rates: SORA Explained

Before we go further, it’s worth understanding what’s really pulling your mortgage rate around, because it isn’t some local central bank setting a policy rate the way the Fed or the Bank of England does.

The Monetary Authority of Singapore (MAS) doesn’t set interest rates directly at all. Instead, it manages the Singapore Dollar against a basket of currencies, known as S$NEER, to keep inflation under control. That means Singapore’s interest rates are mostly imported from overseas, shaped by global markets and, more than anything else, by what the US Federal Reserve is doing.

Most floating-rate home loans here are pegged to SORA, short for Singapore Overnight Rate Average. It’s the benchmark that took over from SIBOR a few years back. Banks then add their own margin on top, usually up to around 1%.

So when the Fed moves, SORA tends to follow within a few months. And once SORA moves, your mortgage rate isn’t far behind.

Singapore Mortgage Rates in 2026: Where Things Actually Stand

Here’s where things sit right now, and it’s a very different world compared to 2023.

Metric | 2023 Peak | Mid 2026 |

3-Month Compounded SORA | Above 3.5% | Roughly 1.0-1.2% |

2-Year Fixed Home Loan | Around 3.10% | From approximately 1.40% |

Floating Rate (SORA + spread) | Above 4.0% | Roughly 1.05-1.55% |

HDB Concessionary Rate | 2.6% | 2.6% (unchanged) |

Three-month SORA dropped from around 3% at the start of 2025 down to roughly 1.2% by year end, and it’s basically held steady near that level heading into 2026. Bank economists mostly expect it to stay somewhere between 0.7% and 1.2% for the rest of the year, though there’s some chance of a small bump up if inflation surprises on the upside.

That’s a big shift if you’re financing a home now versus someone who locked in a rate two or three years ago.

Fixed vs Floating: Which Makes Sense in This Rate Environment

This question comes up in almost every conversation we have with buyers right now, and there’s no single right answer. It really comes down to how long you plan to hold the property.

Fixed Rate | Floating Rate | |

Best for | Buyers who want payment certainty | Buyers who expect rates to fall further or plan to sell within 2 years |

Current range (2026) | ~1.40-1.80% | ~1.05-1.55% |

Risk | You may miss out if rates drop further | Payments rise if SORA climbs back up |

Typical lock-in | 2-3 years | Reprices quarterly (3M SORA) |

The gap between fixed and floating rates is tighter than it’s been in years, sometimes as little as 0.15-0.40%. Because of that narrow spread, a good number of buyers are just picking fixed for the peace of mind, even knowing floating might save them slightly more if SORA keeps sliding.

How a 1% Rate Change Hits Your Monthly Mortgage

Percentages don’t mean much until you see them as real dollars. So here’s what a 1% shift actually looks like on a $1,000,000 loan spread over 25 years.

Interest Rate | Approx. Monthly Payment | Total Interest Over 25 Years |

1.5% | ~$4,000 | ~$200,000 |

2.5% | ~$4,480 | ~$344,000 |

3.5% | ~$5,000 | ~$500,000 |

One percentage point on a $1 million loan works out to roughly $480 more (or less) every month, and close to $144,000 across the full loan tenure. That’s really why interest rates get so much attention in the first place, even when their actual pull on the sale price is far weaker than people assume. Want to see your own numbers? Run them through our mortgage affordability calculator before you sign anything.

The 5 Ways Interest Rates Actually Move the Market

Interest rates ripple through the property market in a few different ways, and they don’t all pull in the same direction at the same time.

- Mortgage affordability. Lower rates shrink monthly repayments, which pulls more buyers into the market and usually bumps up transaction activity.

- Investor behaviour. When bonds and savings accounts barely pay anything, property starts looking like the better option, so money flows that way. Raise rates, and that comparison flips.

- Housing market activity. Cheaper financing speeds up decisions. That family who’d been “thinking about upgrading” for two years finally pulls the trigger.

- Speculation. Cheap money used to fuel quick flips. These days, Singapore’s Seller’s Stamp Duty (SSD) has mostly shut that door, regardless of where rates land.

- Broader economic conditions. Rates usually climb when the economy’s strong and fall when it needs a boost. That underlying backdrop often matters more than the rate number itself.

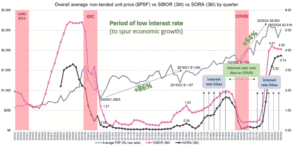

21 Years of Data: Interest Rates vs Property Prices in Singapore

Here’s where the neat little theory falls apart. Line up Singapore’s Property Price Index against interest rates from 2002 to 2023, and the pattern is inconsistent, to put it mildly.

Period | Interest Rate Trend | Property Price Trend |

2004-2006 | Rising | Rising |

2007 | Peaked near 6% | Prices hit an all-time high by Q1 2008 |

2008 | Falling sharply | Falling |

2009-2016 | Low | Rose roughly 86% over the period |

2017-2019 | Rising | Rising |

2019-2020 | Falling | Rising |

2020-2021 | Low | Rising |

2022-2023 | Rising sharply | Still rising |

Three out of these eight periods show rates and prices climbing together, not moving apart like they’re supposed to. If interest rates alone controlled Singapore property prices, that shouldn’t be possible.

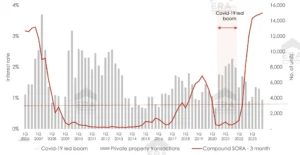

Interest Rate vs Transaction Volume: The Correlation That Actually Holds

Where interest rates actually do show a consistent pattern is with transaction volume, not with price.

Fourteen straight years of low rates, from 2008 to 2022, lined up with strong buying and selling activity for most of that stretch. When rates go up, people don’t usually accept lower prices for their homes. They just take longer to find a buyer, and fewer deals close overall.

That distinction matters if you’re trying to time a purchase or sale around rate movements. A high-rate period usually means a quieter market, not a cheaper one.

The 3 Things That Actually Move Singapore Property Prices

Based on the data, interest rates are just one piece of the puzzle, and probably not even the biggest one. The Singapore government holds three levers that carry more weight:

- Land supply, through Government Land Sales (GLS), which decides how many new units hit the market each year.

- Immigration policy, since Singapore’s population is targeted to grow from roughly 5.5 million toward 6.9 million by 2030, with more Permanent Residents adding to housing demand along the way.

- Cooling measures, including Additional Buyer’s Stamp Duty (ABSD), Total Debt Servicing Ratio (TDSR), and Loan-to-Value (LTV) limits, which throttle demand directly no matter what interest rates are doing.

Land here is genuinely scarce and tightly controlled, so these three factors tend to outweigh rate movements when it comes to actually deciding where prices go.

2026-2027 Price Outlook: Three Scenarios

Nobody’s got a crystal ball on this one, so scenarios make more sense than pretending we can nail down a single number.

Scenario | Interest Rate Path | Likely Price Impact |

Bull case | Fed cuts more aggressively, SORA drops further | Prices could rise 5-8% over 2026-2027, led by OCR and RCR |

Base case | SORA stabilises near current levels through 2026 | Most agencies forecast 2-5% growth for 2026 |

Bear case | Inflation surprises push rates back up | Price growth moderates further, transaction volume slows |

Most of the big property consultancies are sitting in the base case camp right now, forecasting private home prices to rise somewhere in the low to mid single digits for 2026. That’s being driven by steady owner-occupier demand and better affordability, not some aggressive rate-cutting cycle.

What This Means If You’re Buying, Selling, or Refinancing Right Now

- Buyers: stress-test your budget against rates 1-2% higher than today’s offer, not just today’s rate. Fixed lock-ins run out eventually, and floating rates move.

- Existing homeowners: if your current package sits noticeably above the roughly 1.40-1.95% range on offer now, refinancing could save you thousands a year.

- Sellers: a lower rate environment usually pulls more buyers in and shortens how long your listing sits, even if it doesn’t push your final price up.

- Investors: weigh rental yield against your total financing cost carefully. Cheaper mortgages help your cash flow, but yield compression is a real risk if new supply floods in.

Making Sense of It Before You Commit

Interest rates matter, sure, but they’re not the whole picture. Treating them as the single factor behind a buy or sell decision is where a lot of people go wrong. Land supply, population growth, and cooling measures have shaped Singapore property prices far more consistently over the past twenty years than interest rates ever have.

Trying to figure out if now’s the right time to buy given where rates sit? Our property consultation walks through your actual numbers, financing options, and timing, not generic advice. And if you want a longer-term view that factors in GLS supply, population trends, and where cooling measures might head next, it’s worth talking to a Singapore property investment advisor before you commit either way.

For more context on where the broader market stands, check out our breakdown of the major impacts on Singapore’s property market and our take on whether property prices will drop. Both pair well with what we’ve covered here.

At SG Luxury Condo, we keep a close eye on SORA, GLS tenders, and cooling measures, not because rates are the whole story, but because understanding how all three levers work together is what actually helps you time a purchase right. Browsing luxury condos for sale in Singapore and want a clearer read on where things stand today? We’re happy to walk through it with you.